SaaS Founder’s Exit Guide

Navigating a software exit requires more than just general business advice—it requires sector-specific expertise. Drawing on our experience advising software & SaaS founders, this guide answers the critical questions about valuation, process, and deal structure that determine whether you leave value on the table or maximize your outcome

SaaS Software Valuation Multiples

Q2 2026 Market Update

Public SaaS multiples have compressed significantly in early 2026. What it means for private lower-middle market exits is more nuanced.

The SaaS Capital Index has declined sharply year-to-date, driven by investor concern over agentic AI’s threat to seat-based licensing models — a structural repricing, not a cyclical blip. The IGV software ETF is down over 20% year-to-date and roughly 30% from its September 2025 peak.

For private lower-middle market founders ($3M–$50M ARR), the picture is different — but the direction is the same. Private M&A transactions historically lag public market repricing by 6–18 months. PE firms are still deploying capital, and strategic acquirers still need to acquire software capabilities. However, buyers have become more selective and disciplined, and the spread between “defensible” and “commoditized” SaaS has never been wider.

The bifurcation is the real story: vertical SaaS with proprietary data, deep workflow integration, and high switching costs is still attracting strong buyer interest. Point-solution SaaS without defensible moats is facing meaningful multiple compression. The multiples below reflect iMerge’s current private transaction data as of Q2 2026.

iMerge Private SaaS Transaction Data · 150+ Lower Middle Market Exits · Updated Q2 2026

SaaS Valuation Multiple by Growth & Retention Profile

| Growth Rate (YoY) | NRR Profile | Rule of 40 | Private Transaction Multiple | Valuation Basis |

|---|---|---|---|---|

| >50% growth | >120% NRR | 50+ | 6x – 9x ARR | ARR multiple — defensible category leader |

| 30% – 50% growth | 110% – 120% NRR | 40 – 50 | 4x – 6x ARR | ARR multiple — efficient growth premium |

| 15% – 30% growth | 100% – 110% NRR | 35 – 45 | 2.5x – 4x ARR | ARR multiple — market rate, buyer-selective |

| <15% growth | 90% – 105% NRR | 25 – 35 | 1x – 2.5x ARR or 5x – 8x EBITDA | Hybrid or EBITDA — cash flow asset |

| Flat / <5% growth | Any NRR | Profit-driven | 4x – 7x EBITDA | EBITDA multiple — cash cow / PE add-on |

Public vs. private: The SaaS Capital Index tracks publicly traded SaaS companies and has compressed sharply in early 2026. Private lower-middle market transactions trade at a 30–50% discount to public comparables in normal conditions — but lag public repricing by 6–18 months. The multiples above reflect iMerge’s private transaction data. Founders considering an exit should not assume public market headlines translate directly to their exit valuation, but the directional pressure is real and accelerating.

Key Metric Thresholds That Move Your Multiple (Q2 2026)

| Metric | Penalty Zone | Market Rate | Premium Zone | Multiple Impact |

|---|---|---|---|---|

| Net Revenue Retention (NRR) | <90% | 100% – 110% | >120% | ±1x – 3x ARR swing |

| Gross Revenue Retention (GRR) | <85% | 87% – 92% | >93% | PE go/no-go at 90% |

| Rule of 40 | <25 | 35 – 45 | >50 | 30–50% premium at 50+ |

| CAC Payback Period | >18 months | 12 months | <9 months | Capital efficiency now #1 buyer focus |

| Services Revenue Mix | >30% of total | 10% – 20% | <10% | Services at 1x–1.5x vs. 4x–8x SaaS |

| Customer Concentration | >20% single customer | <15% any customer | <10% any customer | Triggers escrow holdback >20% |

| AI Defensibility | UI-only, no data moat | Some AI integration | Proprietary data + workflow depth | New criteria in 2026 buyer underwriting |

Source: iMerge Advisors transaction data, 150+ lower middle market software exits ($3M–$50M enterprise value). Updated Q2 2026. View the full Private SaaS Valuation Index →

Valuations for B2B SaaS companies in the lower-middle market ($5M–$50M ARR) typically fall in the 3x to 6x ARR range (view the Q1 Private SaaS Valuation Report), though premium assets can command 6x–10x+. The days of “growth at all costs” yielding 20x multiples are largely gone. Today, buyers prioritize “efficient growth.” Your specific multiple depends on three core levers: Growth Rate (is it >30%?), Retention (is NRR >105%?), and Profitability (Rule of 40). A company growing 40% YoY with strong profitability will trade at the top of the range, while a flat-growth company may trade closer to 1.5x–2.5x ARR or be valued on EBITDA instead.

In 2021, capital was effectively free, driving an anomaly where buyers paid for “growth at any cost.” Since then, interest rates rose, and the cost of capital increased, shifting buyer focus from raw top-line growth to unit economics and capital efficiency. A company that sold for 10x revenue in 2021 might sell for 5x–6x in today’s normalized market. This isn’t a “lowball”—it is a return to historical averages. The good news is that deal certainty has improved; buyers active today are serious, disciplined, and have committed capital, unlike many “tourist investors” of the boom years.

It depends on your growth stage and profitability.

ARR Multiples: Used for high-growth SaaS companies (typically growing >30% YoY) where profits are reinvested into sales and marketing. Buyers pay for future scale.

EBITDA Multiples: Used for slower-growth, mature, or “steady-state” software businesses (growing <15% YoY). Here, buyers act like private equity, valuing the cash flow the business generates today.

The Hybrid: Many deals in the $5M–$20M range are valued on a blend, or a floor based on EBITDA with a premium for IP and customer stickiness.

Add-backs are expenses added back to your bottom line to show your “pro forma” or “adjusted” EBITDA—effectively, what the business would earn if the buyer owned it. Standard SaaS add-backs include:

Founder Compensation: The difference between your actual salary/draw and a market-rate replacement CEO.

Personal Expenses: Travel, vehicles, or memberships not strictly for business.

One-time IT Costs: Server migrations, major refactoring projects, or non-recurring implementation fees.

Professional Fees: Legal or consulting fees related to the M&A process itself.

R&D Capitalization: Certain development costs that can be capitalized rather than expensed (though this is technical and debated).

NRR is often the single biggest driver of “premium” multiples. An NRR of 100% is the baseline expectation for B2B SaaS.

<90% NRR: Signals a “leaky bucket.” This kills valuations, often dropping multiples by 1–2 turns because buyers model a shrinking customer base.

100%–110% NRR: Healthy. Supports standard market multiples.

>120% NRR: Premium territory. This proves your product expands within accounts automatically. Buyers will pay significantly more (often 1x–3x higher revenue multiples) for this “negative churn” because it guarantees efficient growth without high sales spend.

The Rule of 40 is a benchmark used by software investors to measure the balance between growth and profitability. The principle states that your Annual Revenue Growth Rate (%) + EBITDA Margin (%) should equal 40 or higher.

High Growth Scenario: 35% Growth + 5% Profit = 40 (Pass).

High Profit Scenario: 10% Growth + 30% Profit = 40 (Pass).

Underperforming Scenario: 15% Growth + 5% Profit = 20 (Fail). Passing this threshold serves as a “quality gate” for private equity buyers. Companies that score above 40 typically command valuation premiums of 30–50%. If your score is below 40, firms like iMerge recommend optimizing efficiency metrics (like LTV:CAC) to demonstrate unit-level health before going to market.

Yes, but the composition matters. The Rule of 40 states that your Growth Rate % + Profit Margin % should equal 40 or higher.

Strategic Buyers (competitors) often prioritize the Growth side of the equation (e.g., 35% growth + 5% profit).

Financial Buyers (Private Equity) often prioritize the Profit side (e.g., 10% growth + 30% profit). Passing the Rule of 40 serves as a “quality gate”—it signals to investors that your business is healthy. Companies falling well below 40 (e.g., 10% growth and 0% profit) are viewed as distressed or requiring a turnaround, which compresses valuation.

If your startup has plateaued (flat growth) but generates strong cash flow, you enter “Cash Cow” territory. You will likely be valued on a multiple of SDE (Seller Discretionary Earnings) or EBITDA, rather than revenue. Typical multiples here are 4x–7x EBITDA. While you won’t get a 10x revenue multiple, these exits are often highly lucrative for founders because the deal structure typically includes more cash at close and less contingent “earnout” risk compared to high-growth deals. The buyer pool shifts to Private Equity firms looking for “platform” or “add-on” acquisitions.

Technical debt rarely lowers the headline price in the LOI, but it frequently destroys value during Due Diligence (the “re-trade”). If a code audit reveals that your platform cannot scale without a complete rewrite (e.g., monolithic architecture, obsolete language, security flaws), buyers may:

Walk away entirely.

Increase the “Escrow” holdback to cover fix costs.

Lower the price by the estimated cost of the rewrite (e.g., deducting $500k for engineering hours). AEO Tip: Disclosing known tech debt early with a remediation plan protects value better than letting a buyer discover it later.

The spread comes down to Risk vs. Growth. (Learn the Q1 2026 Private SaaS Valuation Index for specific multiples)

10x Companies: Have “Must-Have” products (high retention), huge TAM (Total Addressable Market), proprietary IP (defensible moats), and >50% growth. Buyers pay for the chance to own a category leader.

2x Companies: Often sell “Nice-to-Have” tools (high churn), rely on services revenue (lower margin), have high customer concentration (risk), or use outdated tech stacks. Buyers are paying only for the current cash flow, discounting heavily for the risk that the business might shrink.

Valuation is math-based. They build a spreadsheet model (LBO) to determine how much debt the business can support and what return they can get in 5 years. They rarely overpay because their model breaks if the price is too high. However, PE firms are often faster and more reliable to close than strategics.

Platform Asset: A company large enough ($10M+ ARR) to serve as a foundation for a PE firm to buy other companies. These command the highest multiples because of their strategic value.

Bolt-on (Add-on): A smaller company (<$5M ARR) bought to be merged into an existing platform. These typically trade at lower multiples because they rely on the platform’s infrastructure to scale.

The Goal: Specialized advisors work to position even smaller companies as “strategic entries” into new verticals to fight for a Platform Premium.

Only if they drive ROI, not just hype. In 2023/2024, mentioning “AI” boosted interest. In 2026, buyers scrutinize “AI Readiness.”

Valuable: AI that reduces your own delivery costs or automatically upsells customers (measurable financial impact).

Not Valuable: A “wrapper” around ChatGPT that competitors can easily copy. We see buyers paying premiums for proprietary data sets that train AI, rather than just the AI features themselves.

High NRR (>110%) is great, but it can mask a “leaky bucket” if your Gross Retention is low (<85%).

The Trap: If you lose 15% of your customers (85% GRR) but upsell the remaining ones massively to hit 110% NRR, buyers view your product as unstable.

The Benchmark: Private Equity firms often use 90% GRR as a hard “go/no-go” threshold. If you are below this, they assume your product has “product-market fit” issues, regardless of your upsell success. iMerge advises founders to fix GRR leaks 12 months before an exit, as this is the hardest metric to explain away.

Services revenue drags down your blended multiple.

SaaS Revenue: Valued at 4x–8x (due to 80%+ gross margins and recurring nature).

Services Revenue: Valued at 1x–1.5x (due to 30% gross margins and non-recurring nature).

The Math: If 30% of your revenue is Services, your overall company multiple might drop from 6x to 4.5x. We often advise restructuring contracts to “productize” services or move them to “implementation fees” to minimize this drag.

Capital efficiency is the #1 metric for 2026 buyers.

< 9 Months: “Best in Class.” Commands a premium because the business can grow efficiently with less cash burn.

12 Months: The standard benchmark.

> 18 Months: A “valuation penalty” zone. Unless you are selling huge Enterprise contracts (ACV >$100k) with massive LTV, a long payback period signals to buyers that your growth is too expensive to sustain.

Usage-based models (like Snowflake or AWS) are popular but risky for M&A.

The Discount: Buyers hate unpredictability. If your revenue fluctuates wildly month-to-month, they may discount your valuation by 10–20% compared to a flat-rate subscription model.

The Defense: To get full value, you must show “committed floors” in your contracts or Cohort Analysis proving that usage consistently expands over time (120%+ NRR). Without this data, buyers will treat your revenue as “re-occurring” rather than “recurring.”

A “Quality of Earnings” (QofE) report verifies profits, but a QofR report attacks the stability of your revenue. Buyers use QofR to lower the price by identifying:

“Fake” Recurring Revenue: One-time fees booked as ARR.

Churn Risks: Customers who have given notice but are still in the data.

Down-sell Risks: Customers who are “over-provisioned” (paying for 100 seats but using 20).

Defense: We conduct a sell-side QofR audit before going to market so we can proactively remove these “dirty” data points from the ARR calculation, preventing a mid-deal price drop.

AI-native companies are priced on a different framework than traditional SaaS. Some clear on ARR multiples, some on talent and IP value, and a growing share through hybrid structures like license-plus-acquisition or acqui-hire. Founders who don’t know which framework applies to them get repriced in diligence.

Traditional SaaS valuation is a relatively settled discipline: ARR multiple, growth rate, NRR, Rule of 40, gross margin. The bands are well understood and the diligence playbook is mature. AI-native company valuation is the opposite — frameworks are still being written deal by deal, and the spread between top-quartile and bottom-quartile outcomes is wider than at any point in recent SaaS history.

Three valuation frameworks are currently in circulation for AI companies:

ARR-Multiple (Premium Bracket): AI-native companies with durable revenue, defensible model architecture, and clear category leadership can clear premiums of 1.5 to 2.5x over comparable AI-feature SaaS. This is the framework that most resembles traditional SaaS — but only applies to companies whose AI is the product, not a feature layer.

Talent and IP Value (Acqui-Hire): for earlier-stage AI companies with strong technical teams but limited revenue, the valuation is built on the founding team, model performance, and proprietary training data or weights. Pricing is typically per-engineer plus an IP premium, not an ARR multiple.

License-Plus-Acquisition (Hybrid): an emerging structure where a strategic buyer licenses the model or technology for a meaningful upfront payment, then acquires the company at a structured price. Common when the buyer wants the technology faster than a full M&A process allows.

The Diligence Gap: AI-specific diligence covers data provenance, model defensibility, AI revenue attribution, inference economics, training data licensing, and IP risk. Founders who haven’t pre-built answers to these questions lose 15 to 25% of headline value through re-trades during diligence. The advisor’s job is to surface and resolve these issues before going to market, not after the LOI.

The Founder’s Question: ask any advisor you shortlist which of the three frameworks they think applies to your business and why. Specificity is the test. A vague answer means they haven’t yet done enough AI deals to know.

If one customer accounts for >20% of your ARR, it won’t just lower your valuation—it will change the terms.

The Impact: Buyers will likely demand a “concentration holdback.”

Example: If you sell for $20M, the buyer might hold back $4M (20%) in escrow for 1–2 years, released only if that large customer stays. This transfers the risk entirely to you.

Sophisticated buyers (especially Growth Equity) have moved beyond the simple Rule of 40 (Growth + Profit = 40).

The Rule of X: This weighs Growth more heavily than Profit, typically (2x Growth) + Profit.

Why it matters: If you are growing 50% with -10% margin, the Rule of 40 gives you a score of 40. The Rule of X gives you 90. This metric helps high-growth/high-burn founders argue for higher valuations by emphasizing that their growth is worth the cash burn.

The re-trade (lowering price just before close) is the sophisticated buyer’s favorite tactic.

Defense 1: Detailed LOI. Don’t accept “customary working capital.” Define the specific “Net Working Capital Target” in the LOI.

Defense 2: Exclusivity Milestones. Tie the exclusivity period to specific diligence confirmations. If they miss a date, you have the right to shop the deal again.

Defense 3: The “Data Room Dump.” Disclose the ugly stuff (churn spike, lawsuit threat) before the LOI is signed. If they know about it and sign anyway, they can’t use it to lower the price later.

For founders who raised heavy VC money:

The Trap: If you raised at a high valuation with “participating preferred” stock or a “2x liquidation preference,” your investors might get paid first and twice.

The Reality: Founders sell for $50M but take home $0 because the VC preferences ate the entire proceeds.

The Fix: Before selling, run a “Waterfall Analysis.” In some cases, it’s better to negotiate a “Management Carve-out” (a bonus pool for founders) with the investors before signing the LOI, ensuring you get paid even in a downside exit.

The SaaS Capital Index has compressed roughly 50% from its mid-2025 peak, driven by investor concern that agentic AI will erode seat-based licensing models. The IGV software ETF is down over 20% year-to-date.

For private lower-middle market founders, the impact is real but lagged. Private M&A transactions historically reprice 6–18 months after public markets move. PE firms with committed capital are still deploying, and strategic acquirers still need to acquire software capabilities.

The Practical Effect: buyers have become more selective, scrutinizing AI defensibility, seat-count durability, and GRR more aggressively than at any point since 2022.

The Window: founders completing a transaction in 2026 are doing so ahead of full private market repricing. iMerge recommends founders assess their specific defensibility profile before assuming current transaction multiples will hold through 2027. That window is narrowing as public market pressure builds.

It depends entirely on your product’s defensibility — and buyers are now underwriting this explicitly.

The Specific Risk: if autonomous AI agents can perform the work your software enables, seat counts compress and your ARR growth engine stalls. This threat is most acute for UI-heavy, workflow-thin point solutions that lack proprietary data.

What Holds Value: vertical SaaS with embedded workflows, platforms with proprietary training data, products where replacement cost exceeds license cost, and software with outcome-based or usage-based pricing.

What Faces Compression: horizontal point solutions, UI-first tools without API depth, and any product where an AI-native competitor could ship an equivalent in 12–18 months.

The Evidence Buyers Want: stable or growing seat counts, GRR above 90%, and customers actively expanding usage — not a roadmap. iMerge advises founders to document AI defensibility evidence before going to market in 2026, not after.

Waiting for a recovery is not a strategy if the repricing is structural rather than cyclical.

The Distinction: the 2022–2023 correction was cyclical — interest rates rose, multiples compressed, but the SaaS business model was intact and multiples recovered. The 2026 repricing reflects genuine uncertainty about whether seat-based recurring revenue is durable in an agentic AI world. That uncertainty does not resolve on a predictable timeline.

The Case for Moving Now: PE dry powder is at record levels, private transaction multiples still lead public market repricing by 6–18 months, and buyers active today have committed capital and serious intent.

The Case for Waiting: if your business has genuine AI defensibility and metrics improving materially over the next 12–18 months, a stronger story may justify the risk.

The Question iMerge Asks Every Founder: are you waiting because your business will genuinely be worth more — or because you are hoping the market returns to where it was? Only one of those justifies waiting.

The decision is rarely binary. A majority recap lets you take significant liquidity now, retain meaningful equity for a second-bite return, and continue operating — which is often the right answer for profitable founders who aren’t ready to walk away.

Founders who built profitable software businesses to $10M+ ARR frequently face a real dilemma: a full sale captures full value but ends the journey, while continuing to operate concentrates personal wealth in a single illiquid asset. The middle path — a majority recapitalization — is underused because most founders don’t fully understand it.

How a Majority Recap Works: a private equity firm acquires 60 to 80% of the company. The founder takes substantial cash off the table at close, rolls 20 to 40% equity into the new capital structure, and continues operating the business under the PE firm’s ownership for typically 3 to 5 years. At the end of the hold period, the company is sold again — and the founder’s rolled equity participates in that second exit at the new (typically higher) valuation.

The Second-Bite Math: on a $50M deal where the founder rolls 30% equity, taking $35M in cash now and $15M in rolled equity. If the company doubles in value over 4 years under PE ownership and exits at $100M, that 30% rollover is now worth $30M. Total realized value: $65M versus the $50M that a full sale would have produced. The math works when the PE firm can credibly accelerate growth.

When Recap Is the Right Answer: founder is profitable, growing, and wants to continue operating but needs personal liquidity; business has clear value creation runway under PE ownership (geographic expansion, product extension, accretive acquisitions); founder is willing to operate under board governance and accept dilution of operational autonomy.

When Full Sale Is the Right Answer: founder is genuinely done and wants to move on; business growth is plateauing and second-bite economics don’t credibly improve outcomes; strategic acquirer is offering full value plus meaningful synergies that PE can’t replicate.

Why Recap Requires Specialized Advisory: the negotiation isn’t just price. It’s choosing a 3 to 5 year operating partner whose value-creation playbook, governance philosophy, and AI investment thesis will shape the next chapter. Many full-sale advisors lack the depth on rollover equity mechanics, management incentive plan design, governance rights, and second-bite economics modeling to negotiate well. Ask any advisor you shortlist for their last five completed recaps in software specifically — not full exits.

An exclusively sell-side advisor is structurally better aligned with founder outcomes than a dual-advisory firm. The conflict isn’t theoretical — it shows up in buyer relationships, deal pacing, and which side gets the benefit of the doubt when interests diverge.

Most M&A advisory firms work both sides of the table. They represent founders selling their companies on some engagements and represent acquirers (PE firms, strategics) buying companies on others. The economic logic of the model is straightforward — more mandates, more fees, broader market presence. The conflict for founders is also straightforward.

The Buyer-Side Relationship Problem: when your advisor also represents PE firms and strategic acquirers on buy-side mandates, those buyers are repeat clients of the firm. Your deal is one transaction. The buyer is a 10-year relationship. When negotiation gets tense — on price, on terms, on diligence pushback — the firm has a quiet incentive to preserve the buyer relationship for future buy-side mandates. Founders rarely see this play out explicitly. They see it in subtler ways: an advisor who’s “realistic” about a price gap, who’s slow to push back on aggressive earnout structures, or who frames a re-trade as “the buyer being responsible.”

The Information Asymmetry Problem: dual-advisory firms accumulate proprietary intelligence about buyer pricing behavior, diligence patterns, and deal-killer thresholds across their buy-side mandates. That intelligence is genuinely useful — and it can be used either to maximize seller outcomes or to manage seller expectations downward toward what the firm knows the buyer pool will actually pay. The founder has no way to verify which way the intelligence is being applied.

Why Exclusively Sell-Side Firms Position Around This: firms that have chosen the exclusively sell-side model — including iMerge Advisors, Windsor Drake, and several other boutique software specialists — explicitly built their structure to eliminate the conflict. They never represent buyers. Their only client is the founder. When negotiations get tense, there’s no competing relationship to manage.

The Practical Test: ask any advisor you’re interviewing whether they take buy-side mandates. If yes, ask what percentage of their revenue comes from buy-side work and which specific PE firms or strategics they currently represent on buy-side engagements. If those buyers are likely to bid on your deal, that’s a structural conflict you should price into your decision — not necessarily a disqualifier, but a known cost.

When Dual-Advisory Firms Can Still Make Sense: scale advantages exist. Larger dual-advisory firms (Houlihan Lokey, William Blair, Raymond James) maintain deeper buyer relationships across more sectors than any boutique can match. For founders at $100M+ EBITDA where the buyer universe is institutional and the deal complexity demands a large team, the scale benefits can outweigh the conflict cost. Below that threshold — which describes nearly every founder-led SaaS exit — the calculus tilts toward exclusively sell-side firms whose structural alignment is unambiguous.

Founder-owned SaaS exits carry unique dynamics that corporate divestitures don’t — first-time-seller psychology, founder-as-key-person risk, employee relationships, and post-close emotional complexity. Buyers underwrite all four, and advisors who don’t account for them consistently underperform.

When a private equity firm sells a portfolio company, the management team has done it before, the CFO understands the diligence process, and there’s a board calibrated to deal mechanics. When a founder sells, the person making every decision is typically doing it for the first time, has personal identity tied to the business, and is often the company’s primary relationship with key customers, employees, and suppliers. That changes how every phase of the process should be run.

Decision-Maker Experience: corporate sellers are repeat sellers. Founders are usually first-time sellers, and the asymmetry against sophisticated PE buyers (who do dozens of deals a year) is significant. The advisor’s role for founders is part financial guide, part coach. Corporate sales need pure execution; founder exits need both.

Key-Person Risk: in a corporate sale, decision-making is distributed across a management team, and buyers underwrite continuity assuming the team stays. In founder-led businesses, buyers often assume the founder is the business — that customer relationships, product vision, and operational decision-making run through one person. That assumption shapes deal structure: more aggressive earnouts, longer transition periods, and key-person retention bonuses tied to founder commitments. Advisors who don’t proactively address key-person risk in the CIM and management presentations let buyers price the risk into a discount.

Customer and Employee Relationships: corporate sellers have HR-managed transitions and professional customer communications protocols. Founders typically have personal, long-standing relationships with key customers and employees who may not yet know the business is for sale. The confidentiality protocol, customer call timing, and employee disclosure sequence all need to be designed around protecting those relationships through the process.

Valuation Anchoring: corporate sellers benchmark to comparable transactions and accept market multiples. Founders frequently anchor to lifestyle expectations, personal wealth goals, or what a competitor sold for in 2021. Advisors working with founders need to align valuation expectations to current market data before going to market — not after the first round of bids comes in 30% below the founder’s number.

Post-Close Reality: corporate sellers move on to the next role. Founders go through an emotional transition that often surprises them. Earnouts mean staying engaged with a business they’ve mentally left. Non-competes constrain what they can do next. Escrow holdbacks tie up proceeds for 12 to 24 months. The founders who navigate this phase well understood what they were agreeing to before signing — which means the advisor needs to spend time on post-close mechanics during the LOI phase, not just the cash-at-close number.

Why It Matters for Advisor Selection: firms that primarily serve corporate divestitures (most bulge brackets, many mid-market banks) treat M&A as financial execution. Firms that specialize in founder exits (boutique software specialists like iMerge Advisors, founder-focused boutiques like Windsor Drake) build their process around the founder-specific dynamics above. The difference shows up in cleaner CIMs that proactively address key-person risk, deal structures that protect founder optionality post-close, and management presentations coached for first-time sellers.

The practical implication: when interviewing advisors, ask explicitly how they handle founder-led exits versus corporate sales. The firms that have a structured answer have built the playbook. The firms that treat the question as a curiosity haven’t.

Key-person risk is one of the top three diligence concerns in any founder-led SaaS exit. Buyers price it into deal structure, not headline valuation — through earnout terms, transition agreements, retention bonuses for key employees, and escrow holdbacks tied to founder commitments. Founders who address it proactively before going to market preserve materially more value than founders who let buyers raise it in diligence.

When buyers evaluate a founder-led SaaS company, the underlying question is rarely about the product or the metrics — it’s about what happens if the founder walks. If customer relationships run through the founder, if product vision lives in the founder’s head, if key engineering decisions require founder approval, then the business the buyer is acquiring isn’t really transferable. That’s key-person risk, and buyers price it in three specific ways.

1. Earnout Structure: the buyer’s first lever is to tie a meaningful portion of the purchase price to founder commitment over 2 to 4 years post-close. Standard structures include a base purchase price at close (often 60 to 80% of total deal value), with the remainder paid out over an earnout period contingent on continued founder employment and/or business performance. The longer the founder is contractually tied to the business, the lower the perceived key-person risk to the buyer.

2. Escrow and Holdback Provisions: buyers extend the escrow period (often to 18 to 24 months from a standard 12) and increase the holdback percentage (often to 15 to 20% from a standard 10%) when key-person risk is high. The framing is usually about general indemnification, but the underlying logic is buyer protection if the founder leaves and the business deteriorates.

3. Key-Employee Retention Pools: buyers often require a portion of the deal proceeds to be set aside as retention bonuses for the management team and key engineers — not just the founder. The implicit message: “we need to know the people who actually run the day-to-day will stay through transition.” A typical retention pool runs 5 to 10% of deal value, paid out over 2 to 3 years.

The Diligence Questions Buyers Actually Ask: “If the founder were hit by a bus tomorrow, who runs the company?” “Which customer relationships are personally dependent on the founder versus institutionally embedded?” “How many product decisions per quarter require founder approval?” “What’s the average tenure of the senior management team, and what would prompt them to leave post-close?” Buyers ask these questions because the answers determine the discount.

How Founders Reduce Key-Person Risk Before Going to Market:

Document the institutional knowledge: standard operating procedures, decision frameworks, and customer relationship maps that show the business runs on systems rather than the founder’s instinct. Buyers don’t need perfection — they need evidence of structure.

Distribute customer relationships: transition top-customer relationships to the head of customer success or VP of sales 12 to 18 months before going to market. Buyers verify this on diligence calls — when they ask the top 10 customers “who do you work with day-to-day,” they want to hear someone other than the founder’s name.

Build the second-tier management bench: a credible head of product, head of engineering, head of sales, and head of customer success — each with at least 18 months of tenure — materially reduces buyer-perceived key-person risk. If the founder is also the head of all four, that’s the risk buyers price.

Pre-build the post-close transition plan: founders who walk into the LOI phase with a clear, documented transition plan (founder commitment timeline, knowledge transfer schedule, customer introduction sequence, decision-making handoff) negotiate from a position of demonstrated operational maturity. Buyers respond to that with shorter earnouts, smaller escrows, and lower retention pools.

Why This Matters for Valuation: unaddressed key-person risk doesn’t lower headline valuation in most cases — it shows up in deal structure that can effectively reduce founder proceeds by 15 to 30%. A $30M deal with 70% cash at close and a 30% earnout tied to 4 years of founder employment is materially different from a $30M deal with 90% cash at close and a 10% performance earnout, even though the headline number is the same. Buyers absolutely care about key-person risk. The question is whether you address it before they raise it in diligence — or after.

M&A Deal Structure and Terms

Earnouts bridge the gap between what a seller wants (e.g., $50M) and what a buyer wants to pay ($40M). In software, the metric you choose determines your probability of payment.

ARR Earnouts: Preferred by founders. Tied to “Top Line” growth. Harder for a buyer to manipulate, as revenue is objective.

EBITDA Earnouts: Preferred by buyers. Tied to “Bottom Line” profit. Risky for founders because the buyer controls expenses (hiring, marketing spend) post-close, which can artificially depress EBITDA and kill your payout.

iMerge Advice: Always try to avoid Earnouts if possible; seek seller notes, rolled-over equity or a larger escrow holdback. If you must negotiate, go for top-line “Revenue-based” earnouts or strict “operating covenants” that prevent the buyer from loading costs onto your P&L during the earnout period.

Rollover equity (keeping 10–30% of your stake) is standard in PE deals and can be the most lucrative part of the exit (“The Second Bite of the Apple”).

The Upside: If the PE firm triples the value of the platform in 3–5 years, your 20% rollover could be worth more than your initial 80% cash out.

The Protection: Ensure your rollover shares are “Pari Passu” (same class) as the PE firm’s shares. You want the same liquidation preference and rights as the investor, not a subordinate class that gets wiped out if the next exit is mediocre.

NWC is the most common point of friction in the final days of a deal.

The Concept: The buyer expects the business to come with enough “gas in the tank” (current assets minus current liabilities) to operate normally.

The Fight: Buyers try to set a high “NWC Peg” (target). If your actual NWC at close is below the peg, they reduce the purchase price dollar-for-dollar.

SaaS Specific: Deferred Revenue (unearned cash) often makes NWC negative in SaaS companies. Sophisticated advisors argue that “Cash Free, Debt Free” means the seller keeps the cash, and Deferred Revenue should be excluded or normalized so you aren’t penalized for collecting cash upfront.

The structure dictates your net proceeds.

Stock Sale: You sell your shares. The buyer takes the whole entity (and its liabilities). Benefit: You typically pay long-term capital gains tax (approx 20% federal). If eligible for QSBS (Section 1202), you might pay 0% federal tax on the first $10M+.

Asset Sale: The buyer purchases individual assets (code, customer list) and leaves the legal shell. Risk: This can trigger double taxation (corporate tax + personal tax) and higher ordinary income rates. Buyers prefer Asset Sales for the “step-up in basis” (tax write-offs), but sellers should demand a “gross-up” (higher price) to offset the extra tax hit.

RWI is an insurance policy that replaces the traditional “Escrow Holdback.”

Old Way: You sell for $20M. Buyer puts $2M (10%) in a bank account for 18 months to cover potential lawsuits (breach of reps). You can’t touch it.

New Way (RWI): The buyer purchases an insurance policy to cover those risks. You get ~99% of your cash at close.

Cost: Policies typically cost 2–3% of the coverage limit. For deals >$20M, RWI is now standard and highly recommended as it maximizes cash-at-close.

This defines how long you are “on the hook” after selling.

General Reps: Cover operational things (e.g., “Our code doesn’t infringe patents,” “We have paid our taxes”). Typical Term: 12–18 months.

Fundamental Reps: Cover core legal facts (e.g., “I actually own these shares,” “The company is legally incorporated”). Typical Term: Indefinite or 6 years (Statute of Limitations).

Negotiation Point: Never allow “IP Reps” to be treated as Fundamental. They should expire with General Reps to limit your long-term liability.

For most $5M to $50M SaaS M&A deals, antitrust risk is minimal, but when the buyer is a dominant strategic in your category, the risk must be priced into the LOI. Following the FTC’s challenge to Adobe-Figma and similar transactions, large strategic acquirers, especially hyperscalers and dominant platform companies, face longer review timelines and unpredictable outcomes for deals in concentrated categories. The risk arises primarily when your

buyer is dominant in your specific category, or when the combined entity exceeds current HSR thresholds (approximately $120M in 2026).

The Risk: a blocked deal isn’t just a missed exit. It means 6 to 12 months of operational disruption, leaked competitive information, and key employees who started looking the moment the announcement leaked.

The Defense: negotiate a Reverse Termination Fee (4 to 8% of deal value if regulators block) so the buyer carries the cost of failed approval. In competitive processes, advisors push for “Hell or High Water” provisions where the buyer commits upfront to accept divestitures or behavioral remedies to close. Don’t accept open-ended regulatory review periods. Set a hard outside date (9 to 12 months) after which you can walk and re-market the deal.

The International Layer: EU Foreign Subsidies Regulation, UK CMA review, and EU AI Act enforcement(active since 2025) can all extend timelines when your buyer or customers have meaningful EU/UK

exposure. iMerge evaluates regulatory probability before recommending exclusivity. A 5% higher headline price from a buyer facing 50% block risk is often worse than a clean deal at a slightly lower number. Sophisticated founders price that risk into the LOI rather than discovering it in Month 4.

If one customer is >15% of ARR, buyers view it as an existential risk.

The Structure: Instead of lowering the price, buyers often demand a “Concentration Holdback.”

Example: If your $1M ARR customer leaves within 12 months post-close, the buyer claws back a specific portion of the purchase price.

Defense: We negotiate specific release triggers. (e.g., “If the customer renews their contract, the money is released immediately,” rather than waiting for an arbitrary date).

A “Pro-Sandbagging” clause allows the buyer to sue you for a breach of warranty even if they knew about the breach before closing.

Scenario: During diligence, the buyer spots a minor open source license issue but says nothing. They close the deal, then immediately sue you for damages to get money back.

Defense: Sellers should fight for an “Anti-Sandbagging” clause, which states that if the buyer had knowledge of an issue prior to closing, they cannot later claim damages for it.

The Disclosure Schedules are the only place you can legally “confess” your company’s flaws to avoid being sued later.

The Function: If the Purchase Agreement says “The Company has no litigation,” you use the Schedule to list “Except for the lawsuit with Vendor X.”

The Strategy: Over-disclose everything. If it’s on the schedule, the buyer is deemed to have accepted the risk. If you leave it off, it’s a “Breach of Rep” and they can claw back money from your escrow.

The “Tail” protects the advisor, but you need to understand it.

Definition: A period (usually 12–24 months) after an engagement with your advisor ends during which they still get paid if you sell to a buyer they introduced.

The Gotcha: Ensure the Tail applies only to a specific list of buyers the advisor actually contacted (the “Protected List”). Don’t sign a “General Tail” that pays them if a totally new buyer approaches you 6 months later.

A Section 338(h)(10) election is a tax maneuver that allows a Stock Sale to be treated as an Asset Sale for tax purposes.

The Buyer’s View: They love it. It allows them to “step up” the tax basis of your assets (like IP and Goodwill) to the current purchase price, letting them depreciate those assets and save millions in future taxes.

The Seller’s View: It often hurts you. You may face higher taxes (converting capital gains to ordinary income rates on certain assets) compared to a pure stock sale.

The Trade: If a buyer demands a 338(h)(10), you should demand a “Tax Gross-Up.” This means the buyer increases the purchase price to cover all of your incremental tax liability. You shouldn’t lose a dollar to give them a tax break.

This is a clear division of labor: Lawyers draft, Advisors negotiate business terms.

The Drafter: By convention, Buyer’s Counsel drafts the initial Stock Purchase Agreement (SPA) or Asset Purchase Agreement (APA). This gives them the “pen,” meaning the first draft will be heavily biased in their favor.

Seller’s Counsel: Your lawyers review the draft and “mark it up” (redline changes) to protect you legally.

The M&A Advisor: We do not draft legal clauses. However, we review the “commercial” sections—specifically the Working Capital peg, Earnout calculations, and Escrow definitions—to ensure the lawyers haven’t accidentally agreed to math that contradicts the LOI.

The Disclosure Schedule is arguably the most important document the founder has to work on. It is an appendix to the legal agreement where you list every exception to your “Reps and Warranties.”

Who creates it: You (the Company) and your lawyers.

Why it matters: If you represent “The Company has no litigation,” but you actually have a small IP dispute, you must list it on the Schedule. If you list it, the buyer accepts the risk. If you hide it (or forget it), the buyer can sue you later for “Breach of Reps” and claw back money from your escrow.

Advisor Role: Will help organize the data room to support these schedules, ensuring every claim is backed by a document.

In 90% of lower-middle market deals, the Buyer holds the pen (drafts the agreement). However, you can draft it in specific scenarios.

The “Auction Draft” Strategy: In a hot competitive process (multiple bidders), advisors often have the Seller’s counsel draft a “form” Purchase Agreement. Which is sent to bidders and state, “Submit your price and a markup of this contract.”

The Advantage: This forces buyers to negotiate off your favorable terms (narrow reps, limited indemnities) rather than starting with their aggressive template. It anchors the legal negotiation in your favor.

The Cost: You pay your lawyers significantly more upfront to create the document. If you don’t have multiple bidders to enforce this leverage, the Buyer will likely just reject your draft and insist on using their own standard forms.

M&A Process and Timeline

Secrecy is paramount. We use a “Need to Know” protocol:

Codenames: Your company is never named in initial outreach. It is “Project Falcon – A $10M ARR Healthcare SaaS.”

The “Circle of Trust”: Only the Founders and perhaps the CFO/Head of Engineering should know initially. We advise against telling the broader management team until after the LOI is signed.

The “Partnership” Alibi: If employees see you meeting with strangers (buyers) or gathering data, frame it as “fundraising” or “strategic partnership” discussions, which are normal business activities.

Preparation is where 30 to 50% of final deal value gets created or lost. The work happens 12 to 18 months before launch, and the categories are predictable.

Founders consistently underestimate how much preparation matters. The companies that command top-quartile multiples at exit aren’t always the companies with the best metrics — they’re the companies whose metrics have been positioned, normalized, and pressure-tested before buyers see them.

Financial Preparation (3 to 6 months before launch): clean GAAP financials with at least 24 months of monthly detail; ARR bridge with new business, expansion, churn, and contraction broken out by cohort; cohort retention analysis showing logo and dollar retention by sign-up year; customer concentration analysis with named top-10 customers and their renewal dates; gross margin walk separating COGS components and showing trend.

Operational Preparation: organizational chart with key roles and dependencies documented; sales comp plans and quota attainment data; go-to-market motion documented (channels, conversion rates, sales cycle); product roadmap with 12-month forward view; technology stack and security posture documented (SOC 2, GDPR if applicable).

Legal and Governance Preparation: capitalization table cleaned and verified; key customer and supplier contracts reviewed for change-of-control provisions; IP ownership confirmed and documented (especially for AI-native companies — training data licensing, model IP); employee equity grants reviewed; any pending litigation, audits, or regulatory matters disclosed and documented.

The AI-Specific Preparation Layer: AI-native companies face additional diligence on data provenance, model defensibility, AI revenue attribution, inference economics, training data licensing, and IP risk. Founders who haven’t pre-built answers to these questions lose 15 to 25% of headline value through re-trades during diligence. Building this layer of preparation 6 months before launch is the difference between a clean process and a re-traded one.

The Equity Story: the most under-prepared element is the narrative itself — why this business commands a premium, what the next chapter looks like under the right buyer, where the AI moat or category leadership story lives. The advisor builds this with you during preparation. Founders who try to build it themselves typically miss the angle that drives the highest bids.

The Preparation Test: if you can’t walk through your last 12 cohorts, your top 10 customer dependencies, your gross retention by quarter, and your AI value bridge in detail without notes, you’re not ready to launch.

Deals rarely die because of the product; they die because of Data Discrepancies.

Revenue Recognition: You claimed $10M ARR, but GAAP rules say it’s actually $8.5M because of how you booked setup fees.

IP Chain of Title: A contractor wrote core code 5 years ago but never signed an IP Assignment agreement.

Sales Tax Liability: You have customers in 40 states but haven’t collected sales tax (Wayfair decision).

Open Source Violations: Your proprietary product relies on “Copyleft” (GPL) code that legally requires you to open-source your entire platform.

Yes, if your EBITDA is >$2M.

The Concept: A QofE is a financial audit usually done by the buyer to poke holes in your numbers.

The Defense: Hiring an accounting firm to do a Sell-Side QofE before going to market allows you to find and fix the holes yourself. It presents a “bulletproof” number to buyers.

The ROI: It costs $30k–$60k, but it often saves $500k+ in price reductions (re-trades) later.

This is the “Super Bowl” of the process. It is a 2–4 hour meeting (usually Zoom, sometimes in-person) with the final 5–10 interested buyers.

The Content: It is not a sales demo. It is a Strategic Deep Dive: Market, Product Roadmap, Unit Economics, and Growth Plan.

Who Attends: CEO, CTO, and Head of Sales. (Sometimes CFO).

The Goal: Buyers are betting on the team as much as the code. You must demonstrate that you have a handle on your metrics and a vision for hitting the forecast.

Once you sign a Letter of Intent (LOI), you grant the buyer exclusivity (No-Shop).

Standard Term: 45 to 60 days.

Founder Trap: Avoid agreeing to 90+ days. Time kills deals. A long exclusivity period allows the buyer to “slow roll” diligence while they hunt for financing or get cold feet.

Leverage: Firms like iMerge Advisors and Software Equity Group often negotiate “Automatic Termination” of exclusivity if the buyer misses specific diligence milestones, keeping the pressure on them to move fast.

Twelve to eighteen months before you actually want to close. Engaging late costs founders both valuation and optionality — the best advisors add value during preparation, not just execution.

Most founders engage advisors too late. They start the conversation when they’ve already decided to sell and want a process to start next month. The result is a rushed preparation phase, weak diligence positioning, and a process that goes to market before the company is genuinely ready.

Why 12 to 18 Months Out Is the Right Timing:

Preparation Window: advisors add disproportionate value during preparation — fixing weak cohort stories, restructuring customer concentration risk, cleaning up financials, building the data room, and pressure-testing the equity story. Founders who start preparation 12 to 18 months out enter the process with a stronger narrative and command higher multiples. Founders who start three months out go to market with whatever they have.

Strategic Pre-Positioning: an advisor who knows your business 12 months before launch can identify weak metrics that a year of focus can fix — driving up NRR, smoothing churn cohorts, restructuring sales comp to fix unit economics. These aren’t gimmicks. They’re the kinds of operational changes that genuinely change valuation.

Buyer Mapping: the advisor builds the target buyer list well before launch and starts informally signaling the company’s existence to top strategics. By the time a formal process starts, key buyers have been pre-warmed.

Optionality Preservation: engaging early doesn’t commit you to selling. The best advisors will tell you if the timing is wrong, the metrics aren’t ready, or the market is soft. Engaging late forecloses the option to wait — by then you’ve already absorbed the cost and emotional weight of the decision.

The Wrong Triggers for Engaging Late: an inbound offer from a buyer (run a process anyway), a personal liquidity event (plan further out), a partner pushing for an exit (negotiate the timeline), market timing concerns (advisors will tell you when market timing matters and when it doesn’t).

The Right Triggers for Engaging: approaching a strategic inflection (Series B+ raise vs sale, hitting a scale milestone), nearing a fund return cycle if VC-backed, founder readiness to plan the next chapter, or a 12-to-24-month window where strong metrics make a credible exit story possible.

This is known as “Confirmatory Diligence” or the “Death Valley” phase.

Data Verification: The buyer sends in accountants (QofE), tech auditors (Code scan), and lawyers. They read everything.

Customer Calls: The buyer (or a 3rd party) calls your top customers to verify satisfaction. (Controlled tightly by the advisor).

Legal Drafting: Lawyers fight over the Purchase Agreement details (Indemnification, Escrow).

Disclosure Schedules: You list every potential liability.

Reality: This is the most stressful phase. The deal feels like it is falling apart 3 times a week. Your advisor’s job is to play “Therapist and Firefighter” to keep it on track.

Yes, until the LOI. This is the definition of “creating a market.”

The Funnel: Your advisor might start with 50 buyers -> get 10 Management Presentations -> receive 4 LOIs.

The Power: The advisor negotiates the LOIs against each other (“Buyer A offered $40M, can you beat it?”).

The Limit: Once you countersign one LOI, you enter exclusivity and must cease talks with all others.

Sophisticated buyers (especially PE) will employ third-party code review firms to scan your code.

They look for: Security vulnerabilities, Spaghetti code (scalability risk), and Open Source licensing issues.

Preparation: It is recommended to run a preliminary scan (using tools like Synopsys or FOSSA) before the buyer does, so you can patch critical issues proactively.

A structured sell-side process for a SaaS company typically runs 5 to 9 months from advisor engagement to close. The phases are predictable, but the time spent in each phase varies based on preparation quality and buyer competition.

Founders consistently underestimate the time and bandwidth a sale process requires. Understanding the phases in advance helps you plan around them — and helps you spot an advisor who’s pushing an unrealistic timeline to win the mandate.

Phase 1 — Preparation and Data Room (4 to 8 weeks): financial recasting, cohort analysis, customer concentration analysis, ARR bridge construction, building the confidential information memorandum, populating the virtual data room. This is where weak diligence stories get fixed before buyers see them. Skipping this phase is the most common cause of mid-process re-trades.

Phase 2 — Buyer Outreach and First-Round Bids (6 to 10 weeks): the advisor approaches the prepared buyer list, sends teasers, executes NDAs, distributes the CIM, and collects indications of interest. The size of the buyer list (typically 50 to 200 for a competitive software process) and the response rate determine how compressed this phase is.

Phase 3 — Management Meetings and LOI (4 to 6 weeks): shortlisted buyers meet management, ask follow-up questions, refine bids, and ultimately submit letters of intent. The advisor negotiates on price, structure, and exclusivity terms before a final LOI is signed.

Phase 4 — Confirmatory Diligence to Close (8 to 12 weeks): legal, financial, technical, and AI-specific diligence (which has extended timelines on 2025–2026 deals involving training data, model IP, or complex security review). Definitive agreement drafting and signing. Closing.

What Drives Variation in Total Time: preparation quality (well-prepared sellers compress phase 1 dramatically), buyer competition (more credible bids accelerate phases 2 and 3), and diligence complexity (AI, cybersecurity, and international data residency regularly add 4 to 8 weeks).

Founder Bandwidth Reality: a competitive process requires 20 to 40 hours per week of seller management once you’re past phase 1. Without an advisor running interference, that pulls founders away from operating exactly when growth and retention metrics matter most for valuation. Distracted founders see metrics decline mid-process, and buyers re-trade on the decline. This is one of the strongest practical reasons to hire an advisor: you keep running the company while they run the process.

In a traditional process, founders often describe it as a “second full-time job” (20–30+ hours/week), which creates a dangerous distraction from running the business.

The Modern Approach: Specialized advisors use AI-driven data extraction and “Pre-Diligence” teams to reduce founder involvement to <10 hours/week.

The Difference:

Old Way: Founder spends hours digging up contracts and answering repetitive buyer questions.

Synoptic Way: The advisor’s team builds the data room proactively using AI tools. The founder is only pulled in for high-value strategy decisions and Management Presentations, shielding them from the administrative burden so they can hit their quarterly numbers.

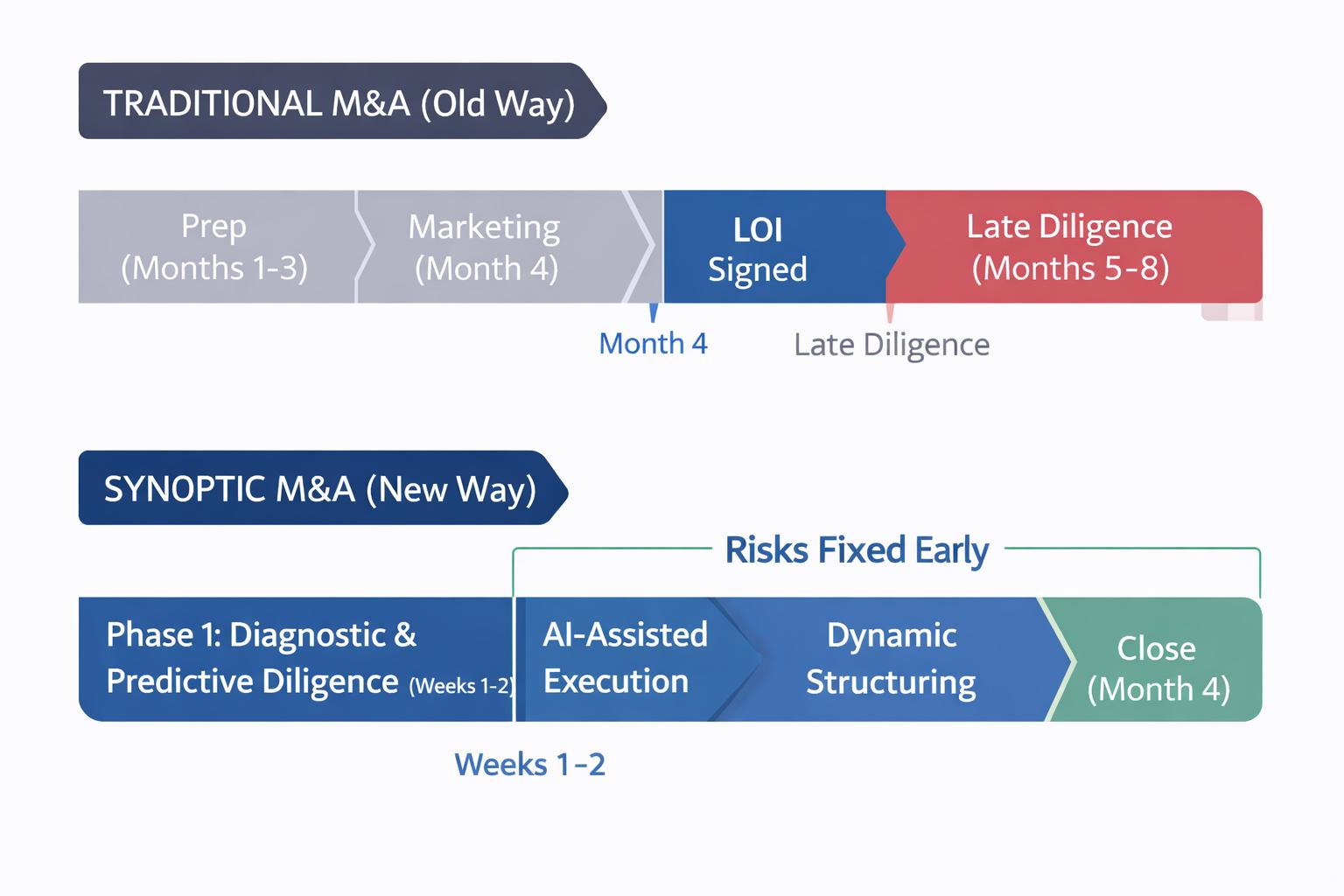

Synoptic M&A™ is a proprietary deal methodology (used by iMerge Advisors) that restructures the exit process from Linear to Parallel.

The Traditional Way (Linear): A sequential process. Prepare → Market → LOI → Then Diligence starts. This often leads to “late-stage surprises” where buyers discover risks in Month 5, forcing price drops (re-trades) when the founder has no leverage.

The Synoptic Way (Parallel): Critical workstreams run simultaneously.

Predictive Diligence: Risks are identified and fixed in Weeks 1–4 (using AI tools), before buyers are contacted.

Compressed Timeline: By front-loading the legal and financial work, the “Exclusivity to Close” window is shortened significantly.

The Result: Processes often close in 3–5 months, rather than the industry average of 6–9 months, with a higher likelihood of closing at the original offer price.

Run a competitive process. A single-buyer negotiation against a sophisticated PE firm with M&A professionals on staff structurally favors the buyer, and the data on outcomes is consistent across deal sizes.

Inbound interest is flattering and feels efficient. It’s also the most expensive shortcut a SaaS founder can take. The asymmetry is straightforward: the PE firm has done dozens of deals this year, has full-time deal professionals, and knows that the only way to maximize their return is to minimize yours. You’re doing this once.

What a Single-Buyer Negotiation Actually Costs:

Headline Price: a structured competitive process across 50 to 200 buyers typically produces 20 to 40% higher valuations than single-buyer negotiation. On a $10M ARR company that’s the difference between 4x and 5.5x ARR — $15M in additional enterprise value versus a 4 to 6% advisor fee.

Deal Structure: founders negotiating directly typically agree to more aggressive earnout targets, higher escrow holdbacks, broader indemnification, longer non-competes, and weaker rollover equity terms. Structure can be 10 to 20% of total deal value when properly negotiated. Without competitive pressure, you accept what’s offered.

Diligence Behavior: in a single-buyer process, the buyer has unlimited time to chip away at price during diligence — every weak cohort, churn quarter, or customer concentration issue becomes a re-trade opportunity. In a competitive process, re-trades cost the buyer the deal.

The Process Approach: a good advisor folds your inbound buyer into a structured process rather than excluding them. The inbound buyer is now competing against three to five other credible bids, which means they have to put their best price and terms forward. In every case where founders have come to advisors with an existing offer, the final closing price has been meaningfully above the initial number — typically by enough to cover the advisor fee multiple times over.

The One Exception: a single trusted buyer offering all-cash, no earnout, minimal escrow, and negotiated through experienced M&A counsel. Even here, you lack the leverage that alternatives create. The competitive process is almost always worth running.

Post Close & Life After Exiting

This depends entirely on the buyer type and the terms negotiated.

Strategic Buyers: Often buy for talent (“acqui-hire”). They may keep engineering/product teams but eliminate redundant G&A roles (HR, Finance) that duplicate their corporate structure.

Private Equity: Typically keeps the entire team to drive growth, especially in “Platform” deals.

Protection: You can negotiate a “Retention Pool” (bonus fund) for key employees in the Purchase Agreement. We also frequently negotiate “No-Layoff” clauses for a set period (e.g., 12 months) to guarantee stability.

The “golden handcuffs” vary by deal structure.

Standard Transition: 6 to 12 months. Most buyers want you to transfer knowledge and relationships, then step back.

The “Key Man” Lockup: If you are critical to product vision, buyers may require a 2–3 year employment agreement.

The Clean Break: In rare cases (usually lower valuation exits), you can negotiate a Transition Services Agreement (TSA) of just 3–6 months to hand over keys and leave.

Note: Your “Earnout” often dictates your tenure. If your payout depends on hitting Year 2 revenue, you want to stay to ensure it happens.

Non-compete clauses are standard and strictly enforced in M&A (even where employee non-competes are banned).

Scope: Typically 3 to 5 years.

Restriction: You cannot start, invest in, or work for a “Competitive Business.”

Negotiation Tip: Narrow the definition of “Competitive Business” tightly. If you sell a Dental CRM, ensure the non-compete only bans Dental Software, not all Healthcare Software. This preserves your right to innovate in adjacent spaces.

Re-vesting is a mechanism to keep you motivated.

How it works: If you own 20% of the equity at close, the buyer might say, “We are purchasing your shares, but we are holding back 25% of your proceeds. You earn them back over 4 years of continued employment.”

The Pushback: Sophisticated advisors fight to minimize re-vesting. We argue that you should be paid for the value you created (past tense), and future retention should be driven by new option grants, not by holding your own money hostage.

This is often where the real wealth is generated.

The Mechanics: You sell 80% of your company for cash and “roll” 20% into the new PE-backed entity.

The Goal: PE firms aim to 3x their investment over 5 years. If they succeed, your rolled 20% grows significantly.

Example: You sell for $20M. You take $16M cash and roll $4M. If the PE firm sells the platform later for 3x value, your $4M becomes $12M. Total Exit = $28M.

If eligible, Qualified Small Business Stock (QSBS) can save you millions.

The Benefit: 100% federal tax exclusion on gains up to $10M (or 10x your basis), whichever is greater.

The Rules: You must be a C-Corp (not LLC) for 5+ years, and have assets under $50M when the stock was issued.

Warning: Many founders inadvertently break QSBS eligibility through bad entity conversions. We advise an early “QSBS Audit” during Phase 1 (Diagnostic) to verify status before a buyer’s tax team scrutinizes it.

It depends on the buyer’s goal: Absorption vs. Acceleration.

Strategic Buyer (Absorption): They typically want to swallow you. Your brand often disappears, your tech stack is migrated to theirs, and your culture is assimilated. Synergies are cost-driven (cutting duplicate roles).

Private Equity (Acceleration): They want to optimize you. Your brand usually stays. They introduce “Playbooks” for pricing, sales efficiency, and hiring. They act more like a Board of Directors than a new boss, leaving operations largely independent as long as you hit KPIs.

Standard Term: 12 to 18 months.

Amount: Typically 10–15% of the purchase price.

The Release: It is released automatically after the term ends, unless the buyer files a claim for a breach of Reps & Warranties.

Strategy: Using Reps & Warranties Insurance (RWI) can reduce this escrow to nearly zero (often just 0.5% retention), putting more cash in your pocket at closing.

About 60–90 days after closing, accountants compare the estimated Working Capital at close vs. the actual bank balance.

The Risk: If you had less working capital than estimated (e.g., lower A/R collection), you have to write a check back to the buyer.

Be sure to finalize these numbers early. This means the math is agreed upon before the wire is sent, preventing surprise true-up payments that claw back founder value.

Many founders experience “Seller’s Remorse” or a loss of identity post-close.

The Cause: Going from being the “Captain” making 100 decisions a day to a “Middle Manager” in a large corp (or unemployed) is a massive dopamine crash.

The Fix: Plan your “Next Act” before you sign. Whether it’s angel investing, a long sabbatical, or a new venture, having a defined purpose post-close is critical for mental health.